THE RISE AND FALL OF A123 SYSTEMS

On 24 September 2009, A123 Systems become a public company trading under the ticker symbol of AONE on the NASDAQ. Its shares soared on the first day of trading closing the day at $20.29 per share, making the company valued at nearly $1.2 Billion. It...

On 24 September 2009, A123 Systems become a public company trading under the ticker symbol of AONE on the NASDAQ. Its shares soared on the first day of trading closing the day at $20.29 per share, making the company valued at nearly $1.2 Billion. It had posted revenues of $36 million during the first six months of 2009, mostly in service revenues. Its marquee investors included names like GE, Qualcomm, and others who, along with the US Department of Energy, had collectively invested over several years in excess of $500 million into the company.

Nearly 3 years later, on 16 October 2012, the company filed for bankruptcy after missing a $2.7 million dollar in interest payment on its outstanding debt. In December of that same year, a bankruptcy judge approved its sale to Wanxiang Group, China’s largest auto parts company, for $257 million. Why would a darling company of the CleanTech industry and Wall Street fall so fast and so hard, and what lessons should the industry heed?

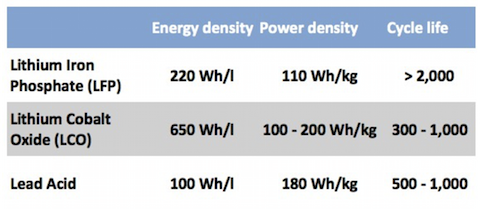

Let’s start with a quick recap of the company’s history. It was formed in 2001 as a spin out from MIT to commercialize a new material system, called nano phosphate, upon which lithium-ion batteries could be built. The background to this new material lied with the safety and reliability issues that plagued the lithium-ion battery industry in the previous decade. The too-frequent fires at battery factories in Asia and product recalls on laptop batteries made the lithium-cobalt-oxide (LCO) material system unsafe at least by reputation, and certainly unsuited for the envisioned electric vehicles of the future. By 2006, the company had collaboration agreements with the US Advanced Battery Consortium (USABC), an automotive consortium bringing together Detroit’s Big Three, along with the US Department of Energy, and was already building battery packs using its proprietary lithium-iron-phoshpate as its primary cathode material. The new batteries were supposedly safer, had very long cycle life (upwards of 2,000 cycles) that was suitable for automotive warranties, and were capable of handling large current spikes — in battery parlance, it is known as power capabilities. But as time would prove, LFP, as this new nano phosphate material system was known, suffered from lower energy densities compared to the material system it was trying to displace.

But any shortcoming on energy density was not sufficient to detract the company from focusing on electric vehicles (EV). By 2008, it had signed agreements with TH!NK to supply batteries to this Norwegian electric-vehicle maker. The next year, it had inked deals with Chrysler, Shanghai Automotive Industry Corp., and Fisker. The future was bright and the potential was enormous. It was time for an IPO.

Underlying this exuberant optimism, especially in 2009 when gas prices hit nearly $5 per gallon and electrification of cars was the future, were some weak fundamentals. Yet, they were either unknown or ignored by many…ultimately, these weak fundamentals led to the demise of the company and its sale. Leaving execution out, these weak fundamentals boil down to choice of technology, product and market.

First, there was and still is a mismatch between the technology of choice, LFP, and the requirements of the EV market. Electric vehicles required a long driving range, which in turn dictated a high-energy density battery technology. LFP has a substantially lower energy density that the LCO material system, and it was doubtful that LFP would improve in time to shrink this gap. In other words, LFP was not suitable to build batteries capable of reaching a 200-mile driving range. For comparison purposes, the energy density of the A123 material system was nearly ⅓ that of the batteries used in the Tesla Roadster — the first model of Tesla Motors. A123, and its list of partner EV manufacturers, were willing to compromise driving range for better reliability and safety. Tesla in contrast, made driving range a key priority for its cars, and elected to improve the safety of the battery through clever engineering designs of its battery pack, i..e, in the mechanical design as well as how the electronic systems safely manage the lithium-ion cells. Nearly a decade later, experience shows that driving range is of paramount importance to drivers of electric cars, and that LCO-based battery packs can be made very safe.

Second, A123 Systems was fundamentally a battery materials company. That’s where its innovation lied. As such, it focused primarily on improving the design and manufacturing of its battery materials. Yet, the battery pack in an electric vehicle was a complex integrated system that brought together both the battery and its materials along with a sophisticated battery management system (BMS), i.e., the electronics and software that control the battery’s performance and reliability. A123 Systems largely left the design of the BMS to its customers. That meant that the overall battery pack system could not be fully optimized as long as its key ingredient subsystems were designed by different parties. In contrast, Tesla elected to design and build the entire battery pack themselves, using a battery cell design (18650) that had been around for at least a decade. In other words, in the complex balance of battery materials vs. system design, where does a company put its emphasis? History now shows us that the system-emphasis proved to be more optimal. Materials in general take a long time — upwards of a decade — and large investment capital to reach commercial maturity. Systems development tend to reach maturity at a faster pace.

Third, or perhaps it should have been first, is cost. The 18650 used in the Tesla models was already being used in millions of laptop computers. It was relatively inexpensive to manufacture. It made sense for, at the time, a nascent electric vehicle company to leverage the scale that the PC industry brought to batteries. In contrast, A123 Systems and all the supporters of LFP had to start from scratch: Build a manufacturing infrastructure, develop an efficient supply chain, establish scalability and ensure reliability. None of these are easy tasks, and they tend to take time and a lot more money. Ultimately, these delays and investments show up as losses in the company’s financial statements.

Lastly, it was about the initial choice by A123 and its partner customers of targeting electric vehicles for the mass market, which meant pushing for affordable car pricing thus introducing serious cost pressures on the supply chain. The electric vehicle market is still in its infancy, even after several years of government incentives and increasing regulation. Therefore targeting electric vehicles for the mass market was a tall order, especially when performance and overall cost were not matching those for traditional vehicles with an internal combustion engine. It greatly increased the challenges that the customers of A123 Systems had to overcome. Over the past several years, we saw both TH!NK and Fisker go bankrupt (Fisker was too acquired by Wanxiang). GM and Ford ultimately chose batteries from LG Chem, a large industrial giant that was willing to underwrite the necessary capital to penetrate Detroit…a luxury that a comparatively small company like A123 could not undertake. Once again, Tesla made a different choice of targeting niche markets, first with an expensive sports car, then going after the high-end luxury market. Both of these choices relaxed the cost constraint and allowed the design and manufacture of an electric vehicle with few if any compromises compared to their combustion-engine counterparts.