Fool's Overture

MWC 2017 is over. The crowds came and saw ideas and innovations. The media covered and reviewed. Awards were made. Yet a sense of public amnesia seemed to hover over the battery safety problems that the Samsung Note 7 brought to surface in 2016...

History recalls how great the fall can be

While everybody's sleeping, the boats put out to sea

Borne on the wings of time

It seemed the answers were so easy to find

Roger Hodgson, Supertramp, from Fool's Overture, 1977

MWC 2017 is over. The crowds came and saw ideas and innovations. The media covered and reviewed. Awards were made. Yet a sense of public amnesia seemed to hover over the battery safety problems that the Samsung Note 7 brought to surface in 2016. Yes, Samsung shows the deep scars of these fateful days. Yes, there is a real fear among the device manufacturers. And yet, the fear and concerns are also accompanied with a sense of paralysis, a sense of a rudderless ship when it comes to safety, and a sense of wishful thinking that the Note 7 fires were an aberration in time that the industry will put behind it.

I will spend today's post to discuss how Samsung's SDI, the primary battery supplier of the Samsung Note 7, is trying to lead its way through the choppy waters of the battery industry. Jun Young-Hyun, an executive who ran Samsung's memory business, became in late February of this year SDI's newest CEO, the company's third in only five years. The information here is specific to Samsung SDI but the intent is to provide an insight into how the incumbents are redefining themselves in the presence of aggressive competition from Chinese battery suppliers.

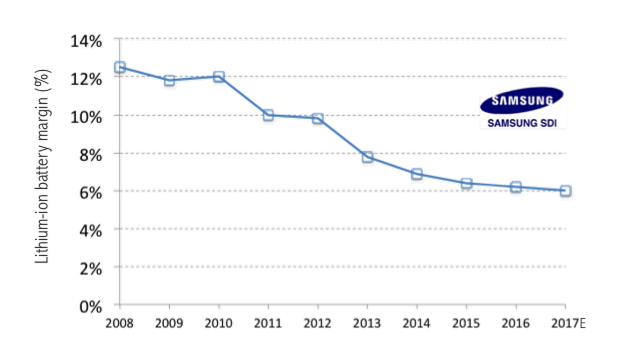

A Goldman Sachs' report charts the decline in operating margin for SDI's lithium-ion battery product lines. Driven primarily by rising competition and decreasing productivity in their cylindrical and polymer batteries, the operating margin dropped by nearly half over the last ten years with little hope of recovery. Samsung SDI's revenues, like many of the incumbents, came primarily from consumer devices including laptops, tablets and smartphones, totaling nearly $2.5 billion in 2016. But these revenues have been flat and are forecasted to stagnate despite rising unit volumes, reflecting the aggressive pricing competition from China.

Panasonic, through its successful relationship with Tesla, was the first to demonstrate that it can shift its revenue base from consumer batteries to automotive batteries. SDI and LG Chem seek to replicate the story.

SDI's growing revenues in the past years in both xEV (encompassing both electrical vehicles and plug-in hybrids) as well as energy storage systems (ESS) reflect that strategy. Samsung SDI forecasts revenues from xEV to exceed $1.5 billion in 2018. The company reports that their ESS line is near breakeven, but that their xEV product line will lose nearly $200 million in 2017.

.jpg)

As LG Chem and SDI increasingly focus their attention on growing their share in xEV and ESS batteries, their Chinese competitors are busy winning market share in consumer devices, and more specifically, in smartphones. Samsung SDI, LG Chem, Panasonic and Sony Energy constituted the vast majority of battery units shipped into consumer devices. In 2016, China-based ATL garnered nearly a third of that market and has become a major supplier to several device OEMs including Samsung Electronics, the maker of the Samsung Galaxy smartphones. Such a scenario was unthinkable only a few years back. Samsung SDI was in effect a sole supplier to Samsung Electronics.

These shifting tectonics in the supply chain carry severe implications to the device OEMs. On the positive scale, more competition means savings to them. But in the process, these device OEMs are losing what once was a comfortable relationship with their battery sister companies. Samsung Electronics' relationship with Samsung SDI allowed it to influence its technology and product roadmap. Samsung SDI provided its sister company with exceptional support. The same can be said of LG and its relationship with LG Chem, and Sony's relationship with Sony Energy. Many pillars of this comfort zone will at least change if not vanish, and that will only cause the device OEMs a lot more anxiety about their battery supply chain. The poor quality and safety record of Chinese battery suppliers is very real. The safety problems of the Note 7 will only amplify these anxieties, even if not publicly displayed.

"History recalls how great the fall can be...It seemed the answers were so easy to find." Timeless words.